The recent period has seen a reassertion of the western countries as major drivers of global growth, and a relative decline of Asia

It’s common to hear analysts talk of “global growth” in a way that suggests that everyone in the world is affected by it equally. Of course, it is well known that this is not true either across or within national economies.

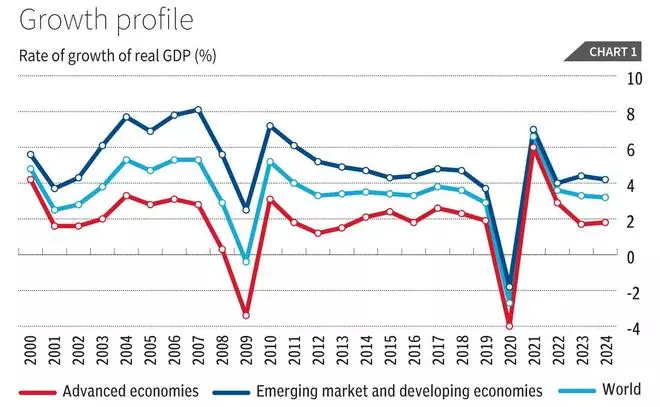

Countries differ hugely in terms of their ability to garner benefits from more rapid global growth or avoid the losses associated with growth slowdown or declines. And within most countries, growing inequality has meant that the rich everywhere have tended to benefit disproportionately from period of economic expansion and avoid the costs of declines. Nevertheless, the sense of broadly similar movements in economic activity across countries persist, and this drives the approach to think in terms of global aggregates. It is certainly true that business cycles have been now remarkably correlated across broad country categories according to levels of development since the turn of the century, as Figure 1 suggests.

US-China rivalry

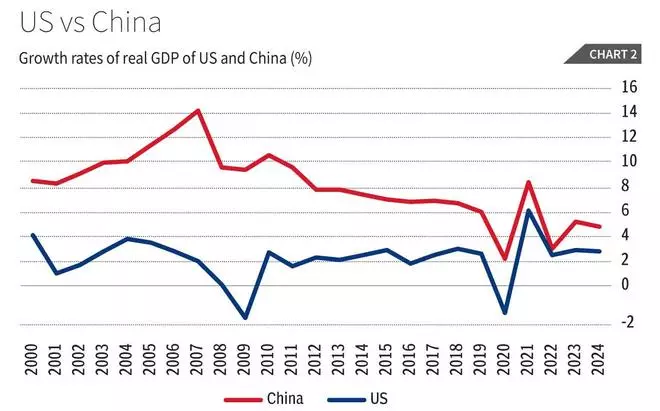

In all discussion of aggregate global economic activity, the two economies that are generally singled out for special attention are the US and China, not only for their current dominant positions, but also for their increasingly intense rivalry. China’s spectacular economic growth over four decades made it the second largest economy in the world by the turn of the century.

Over the past quarter century, China’s economic expansion has outpaced that of the US — but recently the difference has been shrinking, and it is striking that since 2019 the two countries appear to have experienced synchronous economic cycles, unlike in the previous two decades. This reflects the recent growth slowdown in China, but also the very sharp recovery in the US following the pandemic year 2020.

The more rapid rates of growth in some middle and lower income countries — particularly populous ones like China and to a lesser extent India — has given rise to talk of global convergence. But a major part of this is the result of a statistical artefact: the use of Purchasing Power Parity (PPP) exchange rates to measure and compare GDP across countries.

PPP factor

There are many empirical and conceptual concerns with the use of PPP exchange rates, which have now become so widespread. In the current context, one major concern is that PPP exchange rates tend to overstate the GDP of lower income countries.

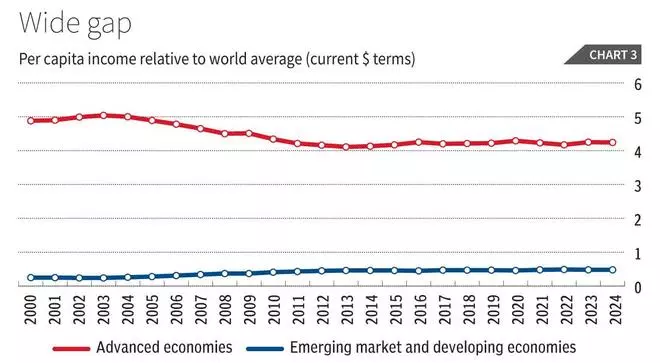

In any case, when looking at the relative economic significance of countries in the global economy, or their contribution to aggregate growth, it makes little sense to use an artificial construct rather than the actual exchange rates that economies face and in which all international transactions occur. Therefore, the figures here use data based on actual, or market exchange rates, not those based on PPP.

This then gives us a rather different picture of economic change over the past quarter century. As Figure 3 shows, convergence of per capita incomes of the major country groups in terms of market exchange rates has been both slow and very little. At the start of the century, the average per capita income in advanced economies was around five times the global average, and this has fallen slightly to around 4.25 times in the most recent period.

By contrast, the average per capita incomes of all developing countries taken together (including China) which began at a quarter of the global average, have still not managed to reach even half of the global average.

Incomes diverging

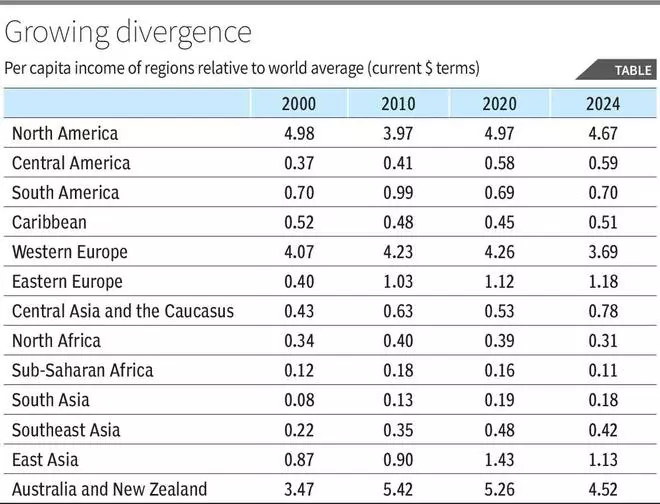

Table 1, describing different regions, shows that the differences across geographies are if anything even greater. Indeed, the African regions show no “convergence” at all in terms of per capita incomes.

Meanwhile, South Asia — which contains India that is generally seen as a country experiencing rapid growth — still remains at per capita income levels of less than one-fifth of the global average, and less than 4 per cent of the North American average.

All this of course excludes internal inequalities, which are known to be especially intense in some regions, and currently account for well more than half of total global income inequality, according to most researchers.

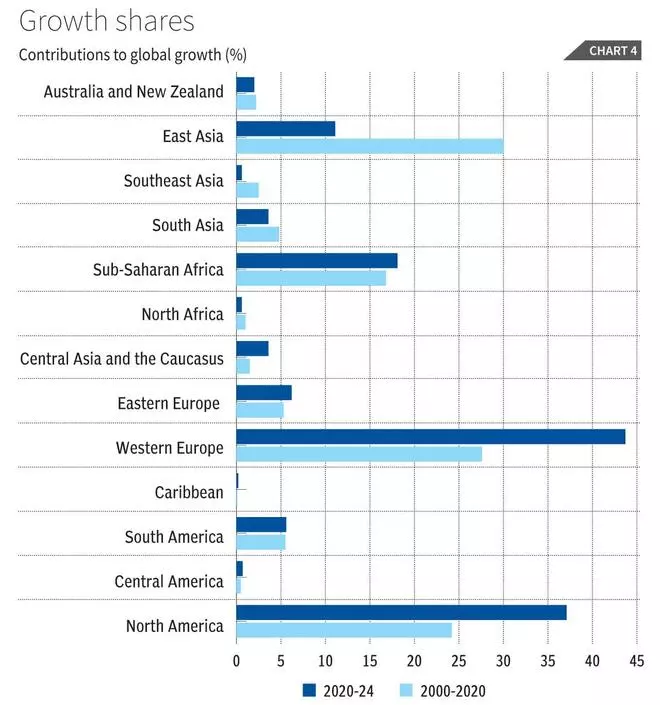

Using the lens of market exchange rates also provides new insights on the contributions to global growth from the different regions. Figure 4 provides data for the first two decades, 2000 to 2020, and then for the four years since the Covid-19 pandemic.

It is evident (as was suggested in Figure1 as well) that the pandemic year marked a shift in growth patterns, such that in the recent period the US and Europe have emerged as the major drivers of global growth, displacing East Asia, which in the previous period had accounted for nearly one-third of global GDP growth.

In the period 2020-24, North America and Western Europe together accounted for more than half (55 per cent) of total global growth, reversing the trend of decline the previous decades.

This was due in no small measure to the very large countercyclical macroeconomic policies (both fiscal and monetary) which had the double effect of enabling faster and larger economic recovery in their own countries, and causing capital outflows, devaluation and debt distress in a range of low and middle income countries.

East, S-E Asia share dips

Meanwhile, East and South-East Asia together accounted for less than 15 per cent of global growth, compared to nearly 35 per cent in the previous two decades.

The ability of the North American and Western European regions to once again reassert their dominance does not reflect inherent economic strength and potential so much as the significance of global currency hierarchies and the ability of these countries to maintain control of the international economic architecture through institutions and legal/regulatory processes established over the previous 75 years.

This is what also enabled them to undertake significantly large fiscal responses during the Covid-19 pandemic, and also provides greater cushion for them in facing future shocks. But nothing lasts forever.

Leave a Comment